Prev

Click the blue text and follow us

✦

JUMBO SHEEN

INVESTMENT

✦

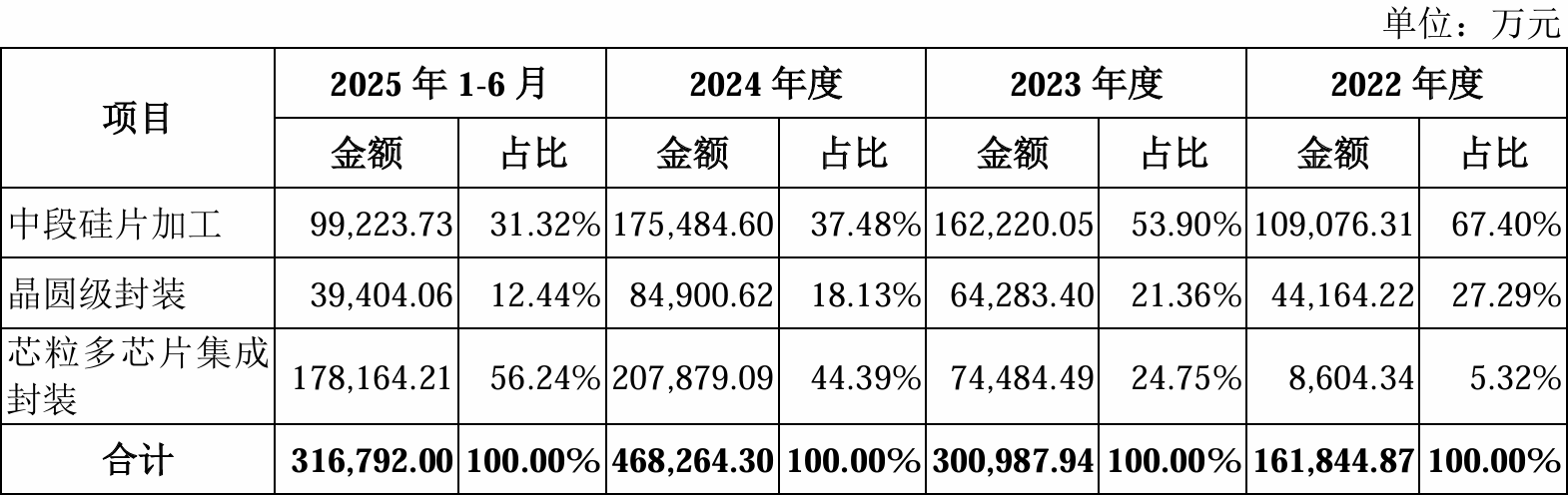

Updates on Invested Projects The 6th deliberative meeting of the Shanghai Stock Exchange Listing Review Committee for 2026 was held on February 24. A total of 1 enterprise was reviewed, and SJSEMI was approved! In the field of middle-end silicon wafer processing, the company is one of the first in Chinese mainland to launch and achieve mass production of 12-inch bumping, and also the first enterprise capable of providing 14nm advanced process bumping services, filling the gap in the high-end integrated circuit manufacturing industry chain in Chinese mainland. Since then, the company has successively achieved breakthroughs in high-density bumping processing technologies for multiple more advanced process nodes, ranking among the international advanced integrated circuit manufacturing industry chain. According to statistics, by the end of 2024, the company owned the largest 12-inch bumping production capacity in Chinese mainland. In the field of wafer-level packaging, relying on its leading middle-end silicon wafer processing capabilities, the company has rapidly achieved the R&D and industrialization of 12-inch large-size wafer-level chip packaging (wafer-level chip scale packaging, WLCSP), including 12-inch Low-K WLCSP for more advanced technology nodes and ultra-thin chip WLCSP with rapidly growing market space. According to statistics, in 2024, the company ranked first in Chinese mainland in terms of revenue from 12-inch WLCSP, with a market share of approximately 31%. In the field of chiplet multi‑chip integration packaging, the issuer has a technical platform layout fully comparable to the world’s leading enterprises. Particularly in 2.5D integration based on TSV Interposer, the most mainstream solution in the industry, the issuer is among the earliest enterprises in Chinese mainland to realize mass production with the largest production scale, representing the most advanced level of Chinese mainland in this technical field, with no technological generation gap compared with the world’s top players. According to statistics, in 2024, the issuer ranked first in Chinese mainland in terms of revenue from 2.5D packaging, with a market share of approximately 85%. In addition, the issuer continues to enrich and improve its technical platforms such as 3D integration (3DIC) and 3D Package, aiming to achieve breakthroughs in more cutting-edge key technologies of the integrated circuit manufacturing industry and create new growth drivers for its future operating performance. The issuer provides one-stop customized advanced IC packaging and testing services for a wide range of chips, including high-performance computing chips, smartphone application processors, radio frequency chips, memory chips, power management chips, fingerprint identification chips, and network communication chips. These products are applied in end markets such as high-performance computing, artificial intelligence, data centers, autonomous driving, smartphones, consumer electronics, and 5G communications, enabling the issuer to deeply participate in China’s digital, information-based, networked, and intelligent development. China has explicitly stated its goal to accelerate the development of the digital economy, deepen the integration of the digital and real economies, and foster internationally competitive digital industrial clusters, which has driven the development of data centers, 5G communications and many other end-use application sectors. Meanwhile, the emergence of multimodal large models such as ChatGPT and autonomous driving technologies such as Robotaxi has promoted artificial intelligence technology from the B-side to the C-side, bringing an exponential increase in computational parameters and a surge in demand for computing power, thus presenting historic growth opportunities for the high-performance computing industry chain. Benefiting from these trends, during the Reporting Period, the issuer’s main business revenue amounted to RMB 161,844.87 ten thousand, RMB 300,987.94 ten thousand, RMB 468,264.30 ten thousand and RMB 316,792.00 ten thousand respectively, showing a rapid growth trend. The composition of the issuer’s main business revenue during the Reporting Period is as follows: Jumbo Sheen Fund SJ Semiconductor Co., Ltd. is a world-leading advanced wafer-level packaging and testing enterprise for integrated circuits. Starting from advanced 12-inch middle-end silicon wafer processing, the company further provides full-process advanced packaging and testing services including wafer-level packaging (WLP) and chiplet multi-chip integration packaging, and is committed to supporting various high-performance chips, especially graphics processing units (GPUs), central processing units (CPUs) and artificial intelligence chips, so as to achieve comprehensive performance improvements such as high computing power, high bandwidth and low power consumption through heterogeneous integration in line with the More than Moore strategy.

SJ Semiconductor Co., Ltd. is a world-leading advanced wafer-level packaging and testing enterprise for integrated circuits. Starting from advanced 12-inch middle-end silicon wafer processing, the company further provides full-process advanced packaging and testing services including wafer-level packaging (WLP) and chiplet multi-chip integration packaging, and is committed to supporting various high-performance chips, especially graphics processing units (GPUs), central processing units (CPUs) and artificial intelligence chips, so as to achieve comprehensive performance improvements such as high computing power, high bandwidth and low power consumption through heterogeneous integration in line with the More than Moore strategy. The sponsor for the issuer’s IPO is China International Capital Corporation Limited (CICC), the auditing firm is RSM China, and the law firm is AllBright Law Offices. Prior to the Offering, the total share capital of the company was 78.65 million shares. The company intends to offer no more than 22.913043 million shares publicly (without considering the over-allotment option), and the total share capital after the Offering will not exceed 101.563043 million shares. The issuer and the lead underwriter may adopt an over-allotment option, which shall not exceed 15% of the offering size without the over-allotment option.

The sponsor for the issuer’s IPO is China International Capital Corporation Limited (CICC), the auditing firm is RSM China, and the law firm is AllBright Law Offices. Prior to the Offering, the total share capital of the company was 78.65 million shares. The company intends to offer no more than 22.913043 million shares publicly (without considering the over-allotment option), and the total share capital after the Offering will not exceed 101.563043 million shares. The issuer and the lead underwriter may adopt an over-allotment option, which shall not exceed 15% of the offering size without the over-allotment option.

Source:Mega IPO;

Disclaimer:The content involved in this article is for sharing and exchange purposes only, and shall not be construed as investment advice. It is provided merely for readers' reference. All copyrights of the quoted content belong to the original authors. If any infringement is found, please contact us for removal.